1. All else equal, which of the following would most likely cause a firm's price-earnings ratio to decline?

A.The level of inflation is expected to decline.

B.The dividend payout ratio increases.

C.The yield on Treasury bills increases.

A B C

C

The risk free rate is a component of ke. ke can be represented by the following: nominal risk free rate + stock risk premium, where nominal risk free rate = [(1 + real risk free rate) × ( 1 + expected inflation rate) ]-1. If the nominal risk free rate increases, ke will increase. The spread between ke and g, or the P/E denominator, will increase. P/E ratio will decrease. P/E = payout ratio/(ke-g).

2. Which of the following statements about stock valuation is least likely correct?

A.If estimated value < the market price, buy the stock : it's under priced.

B.If the expected rate of return > the required rate, buy the stock; it's under priced.

C.If the expected rate of return < the required rate, don't buy the stock; it's under priced.

A B C

A

Buy (sell) a stock when the estimated value is more (less) than the market price.

3. Study the following information, calculate the expected rate of return. index is now selling at $490. market index multiplier is expected to be 5X. index earnings is expected to be $100. dividend payment is expected to be $40.

A.10%.

B.20%.

C.30%.

A B C

A

Step1: Calculate the ending index value = $100×5=$500 Step2: Calculate the expected return. E(R1)=[Dividends + (Ending value - Beginning value)]/(Beginning value)=[40+(500-490)]/490 =0.1 or 10%

4. Which of the following is NOT an assumption of the constant growth dividend discount model (DDM)?

A.The growth rate of the firm is higher than the overall growth rate of the economy.

B.ROE is constant.

C.Dividend payout is constant.

A B C

A

Other assumptions of the DDM are: dividends grow at a constant rate and the growth rate continues for an infinite period.

5. All of the following factors affects the firm's P/E ratio EXCEPT:

A.the expected interest rate on the bonds of the firm.

B.growth rates of dividends.

C.expected dividend payout ratio.

A B C

A

The factors that affect the P/E ratio are the same factors that affect the value of a firm in the infinite growth dividend discount model. The expected interest rate on the bonds is not a significant factor affecting the P/E ratio.

6. Baker Computer earned $6.00 per share last year, has a retention ratio of 55 percent, and a return on equity (ROE) of 20 percent. Assuming their required rate of return is 15 percent, how much would an investor pay for Baker on the basis of the earnings multiplier model?

A.$173.90.

B.Need growth rate to complete calculation.

C.$74.93.

A B C

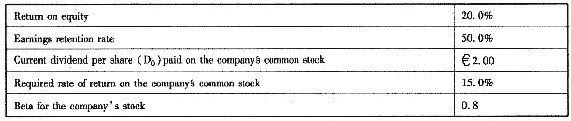

C

g=Retention × ROE=0.55×0.2=0.11 P/E=0.45/(0.15-0.11)=11.25 Next year's earnings E1=E0×(1+g)=6.00×1.11=$6.66 Next years dividend (D1)=E1×Payout ratio =$6.66×0.45=$3.00 P=D1/(k-g)=$3.00/(0.15-0.11)=$74.93

7. Day and Associates is experiencing a period of abnormal growth. The last dividend paid by Day was $0.75. Next year, they anticipate growth in dividends and earnings of 25 percent followed by negative 5 percent growth in the second year. The company will level off to a normal growth rate of 8 percent in year three and is expected to maintain an 8 percent growth rate for the foreseeable future. Investors require a 12 percent rate of return on Day. What is the approximate amount that an investor would be willing to pay today for the two years of abnormal dividends?

A.$1.55.

B.$1.83.

C.$1.62.

A B C

A

First find the abnormal dividends and then discount them back to the present. $0.75×1.25=$0.9375×0.95=$0.89. D1=$0.9375; D2=$0.89. At this point you can use the cash flow keys with CF0=0, CF1=$0.9375 and CF2=$0.89. Compute for NPV with I/Y=12. NPV =$1.547. Alternatively, you can put the dividends in as future values, solve for present values and add the two together.

8. Assume that a firm has an expected dividend payout ratio of 20%, a required rate of return of 9% , and an expected dividend growth of 5%. What is the firm's estimated price-to-earnings (P/E) ratio?

A.5.00.

B.10.00.

C.20.00.

A B C

A

The price-to-earnings (P/E) ratio is equal to (D1/E1)/(k-g)=0.2/(0.09-0.05)=5.00.

9. Given the following estimated financial results, value the stock of Fish Chips, Inc. , using the infinite period dividend discount model (DDM). Sales of $1000000 Earnings of $150000 Total assets of $800000 Equity of $400000 Dividend payout ratio of 60.0% Average shares outstanding of 75000 Real risk free interest rate of 4.0% Expected inflation rate of 3.0% Expected market return of 13.0% Stock Beta at 2.1 The per share value of Fish Chips stock is approximately: (Note: Carry calculations out to at least 3 decimal places. )

10. All of the following variables affect the price-to-cash flow ratio EXCEPT:

A.dividend rate.

B.depreciation rate.

C.growth rate.

A B C

A

Including dividends and capital expenditures would be free cash flow. Normally cash flow from operations is used in price-to-cash flow ratios. Dividends do not affect the calculation.

11. Which of the following would NOT be a reason for market, industry, and company analysis?

A.Firms within a given industry perform differently.

B.The market is generally a very important component of security returns.

C.Single industries perform consistently over time.

A B C

C

The second step in the top-down, three-step valuation process is to identify those industries that will prosper or suffer during the time frame of your economic forecast. You should consider the cyclical nature of the industry under study. Some industries are cyclical, some are contra-cyclical and some are non-cyclical. Finally, your analysis should also account for foreign economic shifts. In general, an industry's prospects within the global business environment determine how well or poorly individual firms in the industry do. Thus, industry analysis should precede company analysis.

12. An analyst gathered the following information about Weston Chemical's stock: Estimated sales per share = $12.19 Earnings before interest, taxes, depreciation, and amortization (EBITDA) = 73% Interest expense per share = $2.07 Depreciation expense per share = $6.21 The tax rate =35% Weston's estimated Earnings per Share (EPS) is closest to?

A.$0.40.

B.$2.54.

C.$3.11.

A B C

A

Estimate earnings per share (EPS) as: [(sales per share) (EBITDA %) - depreciation per share - interest per share] [1 - tax rate ] = ($12.19×0.73-$6.21-$2.07)×(1-0.35)=$0.4022=$0.40.

13. An analyst gathered the following information about a company: Net profit margin 5.0% Total asset turnover 2.0 Total assets/equity 2.5 Beta for the company's stock 1.5 Expected rate of return on the market index 10.0% Risk-free rate of return 5.0% The analyst expects the information above to accurately reflect the future. If the company wants to achieve a growth rate of at least 15% without changing its capital structure or issuing new equity, the maximum dividend payout ratio for the company would be closest to:

A.0.0%.

B.12.5%.

C.40.0%.

A B C

C

The growth rate for the company is the product of the return on equity (ROE) and the retention rate. The retention rate is( 1 - the dividend payout ratio). The ROE for the company is 5.0%×2.0×2.5=25%. The retention rate must be at least 60% to achieve a growth of at least 15% (0.60×25%=15%). If the retention rate is at least 60% , the maximum dividend payout ratio is 40%.

14. An analyst gathered the following information about an industry. The industry beta is 0.9. The industry profit margin is 8%, the total asset turnover ratio is 1.5, and the leverage multiplier is 2. The dividend payout ratio of the industry is 50%. The risk-free rate is 7% and the expected market return is 15%. The industry P/E is closest to:

A.12.00.

B.14.20.

C.22.73.

A B C

C

Using the CAPM: ki =7%+0.9×(0.15-0.07)=14.2%. Using the DuPont equation: ROE =8%×1.5×2=24%. g = retention ratio = ROE=0.50×24%=12%. P/E=0.5/(0.142-0.12)=22.73.

15. The following data pertains to an investor's stock: The stock will pay no dividends for two years. The dividend three years from now is expected to be $1. Dividends are expected to grow at a 7% rate from that point onward. If the investor requires a 17 percent return on their investments, how much will the investor be willing to pay for this stock now?

A.$6.24.

B.$7.31.

C.$8.26.

A B C

B

Time line=$0 now; $0 in year 1; $0 inyear2; $1 in year 3. Note that the price is always one year before the dividend date. Solve for the PV of $10 to be received in two years. FV=10; N=2; I=17; CPT→PV=$7.31.

16. The risk-free rate is 5 percent, the market rate is 12 percent, and the beta of a stock is 0.5, what would happen to the required rate of return if the inflation premium increased by 2 percent? It would:

A.increase to 15.

B.decrease to 8.5.

C.increase to 10.5.

A B C

C

k0=5+0.5×(12-5)=8.5; k1=7+0.5×(14-7)=10.5.

17. All else equal, a firm will have a higher Price-to-Earnings (P/E) multiple if:

A.retention ratio is higher.

B.risk-free rate is higher.

C.the stock's beta is lower

A B C

C

To increase P/E ratio, lower the retention ratio, lower k or increase g. A lower beta would lead to a lower stock risk premium and a lower k.

18. Estimate an earnings multiplier for ABC Company, assuming a dividend payout ratio of 50%, a required return of 12% , and a growth rate of 7%.

A.10.00.

B.12.00.

C.15.57.

A B C

A

The P/E ratio is estimated as the dividend payout ratio divided by the required return minus the growth rate. In this case, 0.50/(0.12-0.07)=10.00.

19. An analyst gathered the following data for the Parker Corp. for the year ended December 31, 2008: EPS2008=$1.75 Dividends2008=$1.40 Betaparker=1.17 Long-term bond rate = 6.75% Rate of return S&P500=12.00% The firm has changed its dividend policy and now plans to pay out 60% of its earnings as dividends in the future. If the long-term growth rate in earnings and dividends is expected to be 5% , the appropriate price to earnings (P/E) ratio for Parker will be:

A.7.98.

B.9.14.

C.7.60.

A B C

C

P/E Ratio =0.60/(0.1289-0.0500)=7.60. Required rate of return on equity will be 12.89 percent =6.75%+1.17×(12.00%-6.75%).

20. General, Inc. , has net income of $ 650000 and one million shares outstanding. The profit margin is 6 percent and General, Inc. , is selling for $ 30.00. The price/sales ratio is equal to:

A.2.77.

B.10.83.

C.0.06.

A B C

A

6% profit margin = $650000/x; x(sales) = $10833333. Sales per share = $10.83m/1000000 = $10.83 per share. P/Sales =$30.00/$10.83=2.77.

21. An analyst gathered the following information about a company's common stock: The value of a share of the company's common stock is closest to: A. . B. . C. .

22. Mamford Industries has solid earnings that are projected to grow steadily into the foreseeable future. Which of the following is TRUE?

A.Mamford is a growth company.

B.Mamford's stock is considered a growth stock.

C.Mamford is a growth company and its stock is a growth stock.

A B C

A

Based upon the information, all we can say is that Mamford is a growth company. The stock may be overpriced and not in a position to grow. The problem gives no information concerning the cyclicality of Mamford Industries.

23. Which of the following statements concerning security valuation is FALSE?

A.The liquidity risk of countries refers to the size and activity of the country's capital markets.

B.ROA times one minus the dividend payout ratio is the firm's sustainable growth rate.

C.If the firm's payout ratio is 40% , has a required return of 12% , and a dividend growth rate of 7%, the firm's price to earnings (P/E) ratio should be 8.

A B C

B

One minus the dividend payout ratio is the firm's retention rate. The sustainable growth rate is the firm's return on equity (ROE) times the retention rate.

24. Assume a company's ROE is 14% and the required return on equity is 13%. All else remaining equal, if there is a decrease in a firm's retention rate, a stock's value as estimated by the constant growth dividend discount model (DDM) will most likely:

A.increase.

B.decrease.

C.not change.

A B C

B

In this case, reduction in earnings retention will likely lower the P/E ratio. The logic is as follows: Because earnings retention impacts both the numerator (dividend payout) and denominator (g) of the P/E ratio, the impact of a change in earnings retention depends upon the relationship of k and ROE. If the company is earning a higher rate on new projects than the rate required by the market (ROE > ke), investors will likely prefer that the company retain more earnings. Since an increase in the dividend payout would decrease earnings retention, the P/E ratio would fall, as investors will value the company lower if it retains a lower percentage of earnings.

25. By bee is expected to have a temporary supernormal growth period and then level off to a "normal," sustainable growth rate forever. The supernormal growth is expected to be 25 percent for 2 years, 20 percent for one year and then level off to a normal growth rate of 8 percent forever. The market requires a 14 percent return on the company and the company last paid a $2.00 dividend. What would the market be willing to pay for the stock today?

A.$52.68.

B.$47.09.

C.$76.88.

A B C

A

First, find the future dividends at the supernormal growth rate(s). Next, use the infinite period dividend discount model to find the expected price after the supernormal growth period ends. Third, find the present value of the cash flow stream. D1=2.00(1.25)=2.50(1.25)=D2=3.125(1.20)=D3=3.75 P2=3.75/(0.14-0.08)=62.50 N=1; I/Y=14; FV=2.50; CPT PV=2.19. N=2; I/Y=14; FV=3.125; CPT PV=2.40. N=2; I/Y=14; FV=62.50; CPT PV=48.09. Now sum the PV's: 2.19+2.40+48.09=$52.68.

26. In the top-down approach to valuation, industry analysis should be conducted before company analysis because:

A.most valuation models recommend the use of industry-wide average required returns, rather than individual returns.

B.the goal of the top-down approach is to identify those companies in non-cyclical industries with the lowest P/E ratios.

C.an industry's prospects within the global business environment are a major determinant of how well individual firms in the industry perform.

A B C

C

In general, an industry's prospects within the global business environment determine how well or poorly individual firms in the industry do. Thus, industry analysis should precede company analysis. The goal is to find the best companies in the most promising industries; even the best company in a weak industry is not likely to perform well.

27. Which of the following statements concerning security valuation is FALSE?

A.Determining the value of a company with supernormal growth requires finding the present value of the dividends during the supernormal growth and adding that to the present value of the stock computed for the period of normal growth.

B.The top-down valuation approach requires an assessment of industry influences on the company's value first, then stock-specific influences.

C.A firm with a 20% return on equity (ROE) and a dividend payout ratio of 30% will have a sustainable growth rate of 14%.

A B C

B

The top-down valuation approach requires an assessment of general economic conditions first, then industry influences on the company's value, and then stock-specific influences.

28. Emanuel Rodriguez, CFO of Monterrey Spikes Sports Goods Inc. , has gathered the following information about the company: 2000 2007 Sales $128.4 million 220.0 million ROA 10% 12% Net profit margin 6% 7% Number shares outstanding 5 million 6 million Rodriguez expects sales in 2008 to grow at the historical compound annual growth of sales from the year 2000 to 2007. For the year 2008, the net profit margin and the number of shares outstanding are expected to remain unchanged from the year 2007. The company's earnings per share (EPS), for the year 2008, is closest to:

29. Use the following information to determine the value of River Gardens' common stock: Expected dividend payout ratio is 45 percent. Expected dividend growth rate is 6.5 percent. River Gardens' required return is 12.4 percent. Expected earnings per share next year are $3.25.

A.$27.25.

B.$24.80.

C.$19.67.

A B C

B

First, estimate the price to earnings (P/E) ratio as: (0.45)/(0.124-0.065)=7.63. Then, multiply the expected earnings by the estimated P/E ratio: $3.25×7.63=$24.80.

30. The top-down approach of security analysis includes:

A.industry analysis.

B.All of these choices are correct.

C.economic analysis.

A B C

B

Economic, industrial, and company analysis, in that order, must all be accomplished in the top-down approach.

31. BIM Technologies Inc. is a large firm in a competitive industry. The company has above-average investment opportunities and its return on investments has been above the company's required rate of return. In addition, BIM has invested heavily in fixed assets and technology to reduce its production costs. The company has also increased its advertising budget substantially to establish a strong brand image for its products. From the above description, BIM is best characterized as a

A.cyclical company that follows a low-cost strategy.

B.speculative company that follows a differentiation strategy.

C.growth company that follows a defensive competitive strategy.

A B C

C

A growth company is a firm with the management ability and the opportunities to make investments that yield rates of return greater than the firm's required rate of return. A company following a defensive competitive strategy attempts to position itself to deflect the effect of the competitive forces in the industry. Examples may include investment in fixed assets and technology to reduce its production costs or increasing advertising budgets to establish a strong brand image for products.

32. An analyst has calculated the following ratios for a firm: Sales/Total Assets: 2.8 Net Profit Margin (%): 4 Return on Total Assets (%): 11.2 Total Asset/Equity: 1.6 The return on equity for this firm would be closest to:

A.4.48%.

B.6.40%.

C.17.92%.

A B C

C

ROE = Net Profit Margin × Sale/Total Assets × Total Assets/Equity =4.00×2.80×1.60=17.92%, Alternatively , ROE = Return on Total Assets × Total Assets/Equity =11.20×1.60=17.92%.

33. All else equal, will a decrease in the expected rate of inflation result in a decrease in the: Real risk-free of return Nominal risk-free rate of return ①A. Yes No ②B. Yes Yes ③C. No Yes A. ①B. ②C. ③

A B C

C

The nominal risk-free rate of return includes both the risk-free rate of return and the expected rate of inflation. A decrease in inflation expectations would decrease the nominal risk-free rate of return, but would have no effect on the real risk-free rate of return.

34. Current dividend per share ( Do) paid on the company common stock $5.00 Required rate of return on the company common stock 15.5% Expected constant growth rate in earnings and dividends 7.5% The value of a share of the company's stock and the leading price/earnings (P/E) ratio, respectively, are closest to: Value of stock Leading P/E ration ①A. $40.13 7.5 ②B. $67.19 8.0 ③C. $67.19 7.5 A. ①B. ②C. ③

A B C

C

The constant growth dividend model and the earnings multiplier model will result in the same value for a share of stock. Using the constant growth model the value is ($5.00) (1.075) or $5.375 divided by the required rate of return minus the growth rate: $5.375/0.08=$67.188. The earnings multiplier is the dividend payout ratio divided by the required rate of return minus the growth rate: 0.6/0.08=7.5.

35. A stock, which currently does not pay a dividend, is expected to pay its first dividend of $1.00 in five years (D5=$1.00). Thereafter, the dividend is expected to grow at an annual rate of 25 percent for the next three years and then grow at a constant rate of 5 percent per year thereafter. The required rate of return is 10. 3 percent. What is the value of the stock today?

A.$20.65.

B.$20.95.

C.$22.72.

A B C

A

This is essentially a two-stage DDM problem. Discounting all future cash flows, we get: Note that the constant growth formula can be applied to dividend 8 because it will grow at a constant rate (5%) forever. It is preferable to do this with the right keystrokes on the calculator but it is a bit tricky. Since the first non-zero cash flow occurs in year 5, we have to communicate this information to the calculator correctly to get the indicated solution. Using the CF function the sequence of keystrokes would be : CF0=0; CF1=0, F1=4; CF2=1.00; CF3=1.25; CF4=1.5625; CF5=40.6471; I=10.3; CPT NPV=$20.647. When we input the first dividend as CF2=1.00, we are telling the calculator that this is really received in the fifth year and it is then discounted correctly. Note that CF5 is made up of two components-the dividend that is paid in year 8=1.253=1.93125 plus the present value of the constantly growing ( at 5% ) perpetuity = . These must be added since they are effectively received at the same point in time.

36. Which of the following statements concerning security valuation is FALSE?

A.An investor may determine the required rate of return for the dividend discount model (DDM) by adding a risk premium to the nominal risk-free rate.

B.In the dividend discount model (DDM), the value of the firm is the present value of all future dividends.

C.An investor can estimate the growth rate for the dividend discount model (DDM) by multiplying the firm's return on equity (ROE) by the firm's dividend payout ratio.

A B C

C

An investor can estimate the growth rate for the DDM by multiplying the firm's ROE by the retention rate, which is one minus the firm's dividend payout ratio.

37. The current price of XYZ Inc. is $40 per share with 1000 shares of equity outstanding. Sales are $ 4000 and the book value of the firm is $ 10000. What is the price/sales ratio of XYZ Inc. ?

A.0.010.

B.10.000.

C.4.000.

A B C

B

The price/sales ratio is (price per share)/(sales per share)=(40)/(4000/1000)=10.0.

38. Assuming that a company's ROE is 12% and the required rate of return is 10%, which of the following would most likely cause the company's P/E ratio to rise?

A.The inflation rate falls.

B.The firm's dividend payout rises.

C.The firm's ROE falls.

A B C

A

The expected inflation rate is a component of ke ( through the nominal risk free rate), ke can be represented by the following: nominal risk free rate + stock risk premium, where nominal risk free rate = [ ( 1 + real risk free rate) ( 1 + expected inflation rate) ] - 1. If the rate of inflation decreases, the nominal risk free rate will decrease, ke will decrease. The spread between ke and g, or the P/E denominator, will decrease. P/E ratio will increase.

39. An analyst gathered the following information about four common stock that all have the same dividend payout ratio:

Stock

Required Rate of Return

Dividend Growth Rate

1

16.4%

7.1%

2

14.1%

9.2%

3

15.3%

4.4%

4

19.1%

8.0%

The lowest earnings multiplier (price earnings ratio) would most likely be associated with stock:

A.2.

B.3.

C.4.

A B C

C

The lowest earnings multiplier is associated with higher (r-g).

40. An analyst gathered the following information about a company: The stock is currently selling for per share. Which of the following best characterizes the: Intrinsic value of the stock type of stock ①A. Cyclical ②B. Speculative ③C. Speculative A. ①B. ②C. ③

A B C

C

Implied dividend growth rate = ROE × RR = 20%×0.5=10% Intrinsic value of the stock: The stock is overvalued; it is a speculative stock.

41. Billie Blake is interested in a stock that has an expected dividend one year from today of $1.50, i. e. , D1=$1.50, D2=$1.75 and D3=$2.05. She expects to sell the stock for $47.50 at the end of year 3. What is Billie willing to pay one year from today if investors require a 12 percent return on the stock.

A.$38.01.

B.$41.06.

C.$52.30.

A B C

B

Find the present values of the cash flows and add them together. N=1; I/Y=12; FV=1.75; compute PV=1.56. N=2; I/Y=12; FV=2.05; compute PV=1.63. N=2; I/Y=12; FV=47.50; compute PV=37.87. Stock Price=$1.56+$1.63+$37.87=$41.06.

42. A stock has a required rate of return of 15%, a constant growth rate of 10%, and a dividend payout ratio of 45%. The stock's price-earnings ratio should be:

A.3.0 times.

B.9.0 times.

C.4.5 times.

A B C

B

P/E=D/E1/(k-g) D/E1= Dividend Payout Ratio = 0.45 k=0.15 g=0.10 P/E=0.45/(0.15-0.10)=0.45/0.05=9

43. Using the one-year holding period and multiple-year holding period dividend discount model (DDM), calculate the change in value of the stock of Monster Burger Place under the following scenarios. First, assume that an investor holds the stock for only one year. Second, assume that the investor intends to hold the stock for two years. Information on the stock is as follows: Last year's dividend was $2.50 per share. Dividends are projected to grow at a rate of 10.0% for each of the next two years. Estimated stock price at the end of year 1 is $25 and at the end of year 2 is $30. Nominal risk-free rate is 4.5%. The required market return is 10.0%. Beta is estimated at 1.0. The value of the stock if held for one year and the value if held for two years are: Year one Year two ①A. $25.22 $35.25 ②B. $27.50 $35.25 ③C. $25.22 $29.80 A. ①B. ②C. ③

A B C

C

ke = Rf+Beta×(Rm-Rf)=4.5%+1×(10.0%-4.5%)=4.5%+5.5%=10.0%. D1=D0×(1+g)=2.50×1.10=2.75 D2=D1×(1+g)=2.75×1.10=3.03 Use DDM to calculate the present value of the expected stock cash flows ( assuming the one-year hold ). P0=[D1/(1+ke)]+[P1/(1+ke)]=[$2.75/1.10]+[$25.0/1.10]=$25.22. Use the multi-period DDM to calculate the return for the stock if held for two years. P0=[D1/(1+k)]+[D2/(1+ke)2]+[P2/(1+ke)2]=[$2.75/1.10]+[$3.03/1.102]+[$30.0/1.102]=$29.80.

44. All else equal, an increase in a company's growth rate will most likely cause its P/E ratio to:

A.increase.

B.not change.

C.decrease.

A B C

A

Increase in g: As g increases, the spread between ke and g, or the P/E denominator, will decrease, and the P/E ratio will increase.

45. An analyst gathered the following financial information about a firm: Estimated EPS $10 per share Dividend payout ratio 40% Required rate of return 12% Expected long-term growth rate of dividends 5% What would the analyst's estimate of the value of this company's stock be?

46. Peter Welsh, CFA, gathered the following information from a company's most recent financial statements ( U.S. $ in millions):

Preferred stock

40

Common stock

120

Additional paid-in capital

30

Retained earnings

190

Treasury stock

(55)

Total shareholders' equity

325

Total number of common shares outstanding

10 million

Tax rate

40%

Welsh also determined that the company uses the LIFO inventory method, but most companies in the industry use the FIFO method. The footnotes to the financial statements indicate that if the company had used the FIFO method, the inventory balance would have been $ 50 million higher than the amount reported on the company's most recent financial statements. If the company's common stock is currently selling for $70 per share, the most appropriate price to book value ratio to use in valuing the company is:

A.2.22.

B.2.03.

C.2.16.

A B C

A

P/B ratio = market value of equity/book value of equity = P/book value per share =70/[325-40+50×(1-40% )]/10=2.22. Book value of equity = common shareholder's equity = (total assets - total liability) - preferred stock.

47. Suppose a stock has a dividend payout ratio of 40 percent, a required rate of return of 15 percent and an expected growth rate of dividends of 10 percent. What is the P/E ratio of the stock?

A.2.667.

B.1.5.

C.8.0.

A B C

C

The P/E ratio is computed as 0.40/(0.15-0.10)=8.0.

48. The earnings multiplier model, derived from the dividend discount model, expresses a stock's P/E ratio (P0/E1) as the:

A.expected dividend in one year divided by the difference between the required return on equity and the expected dividend growth rate.

B.expected dividend payout ratio divided by the sum of the expected dividend growth rate and the required return on equity.

C.expected dividend payout ratio divided by the difference between the required return on equity and the expected dividend growth rate.

A B C

C

Starting with the dividend discount model P0=D1/(ke-g), and dividing both sides by E1 yields: P0/E1=(D1/E1)/(ke-g) Thus, the P/E ratio is determined by: The expected dividend payout ratio (D1/E1). The required rate of return on the stock (ke). The expected growth rate of dividends (g).

49. Which of the following statement is least likely correct? A speculative:

A.stock is usually under priced.

B.company has highly risky assets.

C.stocks have a slight probability of an enormous return.

A B C

A

Speculative stocks are almost always overpriced.

50. Which of the following statements about the constant growth dividend discount model (DDM) in its application to investment analysis is FALSE? The model:

A.is best applied to young, rapidly growing firms.

B.can't be applied when g > K.

C.can't handle firms with variable dividend growth.

A B C

A

The model is most appropriately used when the firm is mature, with a moderate growth rate, paying a constant stream of dividends. In order for the model to produce a finite result, the company's growth rate must not exceed the required rate of return.

. B.

. B.  . C.

. C.  .

.

. These must be added since they are effectively received at the same point in time.

. These must be added since they are effectively received at the same point in time.

per share. Which of the following best characterizes the:

per share. Which of the following best characterizes the: Cyclical

Cyclical Speculative

Speculative Speculative

Speculative

深色:已答题 浅色:未答题

深色:已答题 浅色:未答题